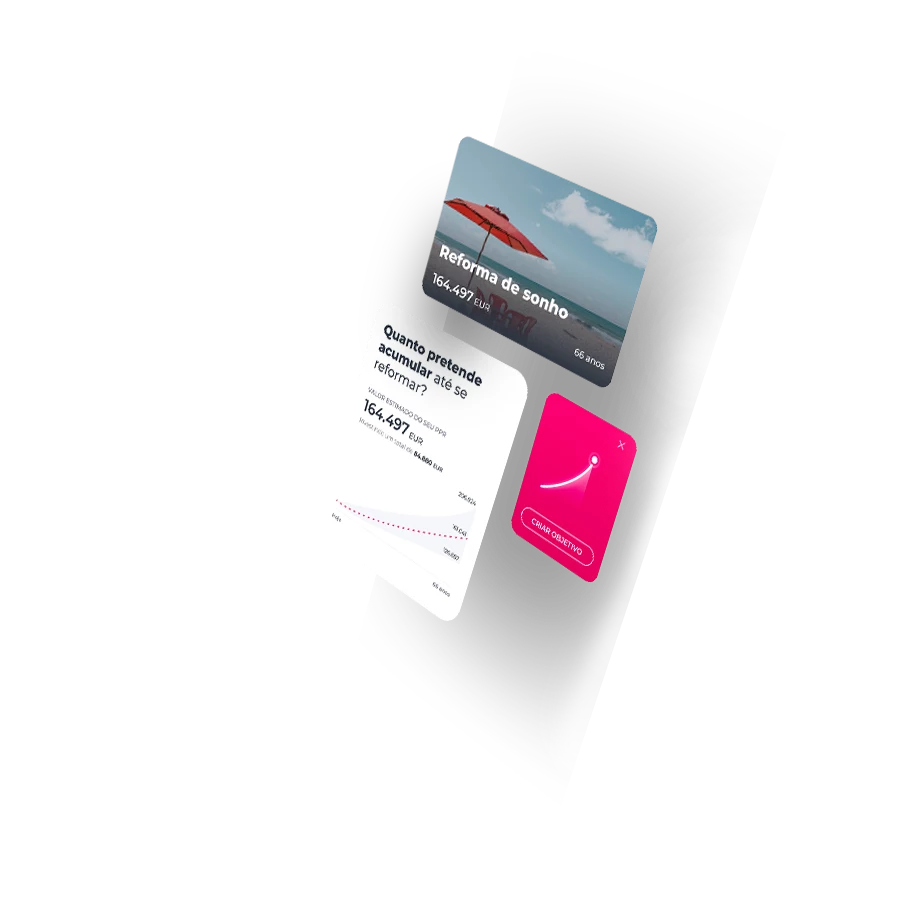

Retirement

Start planning now…

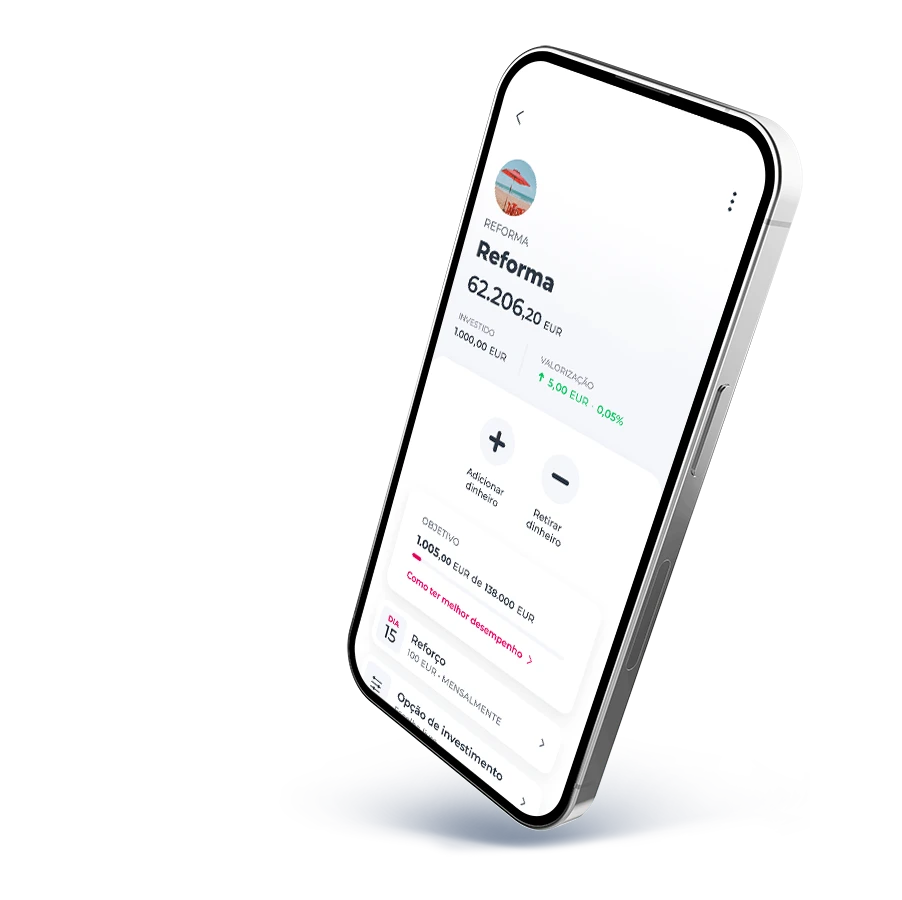

Reforma Ativa 2ª Série

To secure a future of new passions and adventures

Invest in a digital insurance managed by specialists

Invest in a digital insurance managed by specialists

Tax benefits up to €400

Tax benefits up to €400

Invest in a digital insurance managed by specialists

Invest in a digital insurance managed by specialists

Tax benefits up to €400

Tax benefits up to €400

Reforma Ativa 2ª Série

To secure a future of new passions and adventures

Invest in a digital insurance managed by specialists

Tax benefits up to €400

IMGA Crescimento PPR

For those who prefer to start young

Tax benefits up to €400

Up to 100% in stocks

IMGA Poupança PPR

For those who are more conservative

Tax benefits up to €400

Long-term solution

IMGA investimento PPR

For those who prefer risk

Tax benefits up to €400

Early repayment

Rendimento flexível

Boost your retirement savings

Monthly income

Professional management

Compare cards

Greater flexibility

Discover how retirement plans work

Need help?

Need help?

Looking for a branch?

Looking for a branch?

Need to call us?

Need to call us?