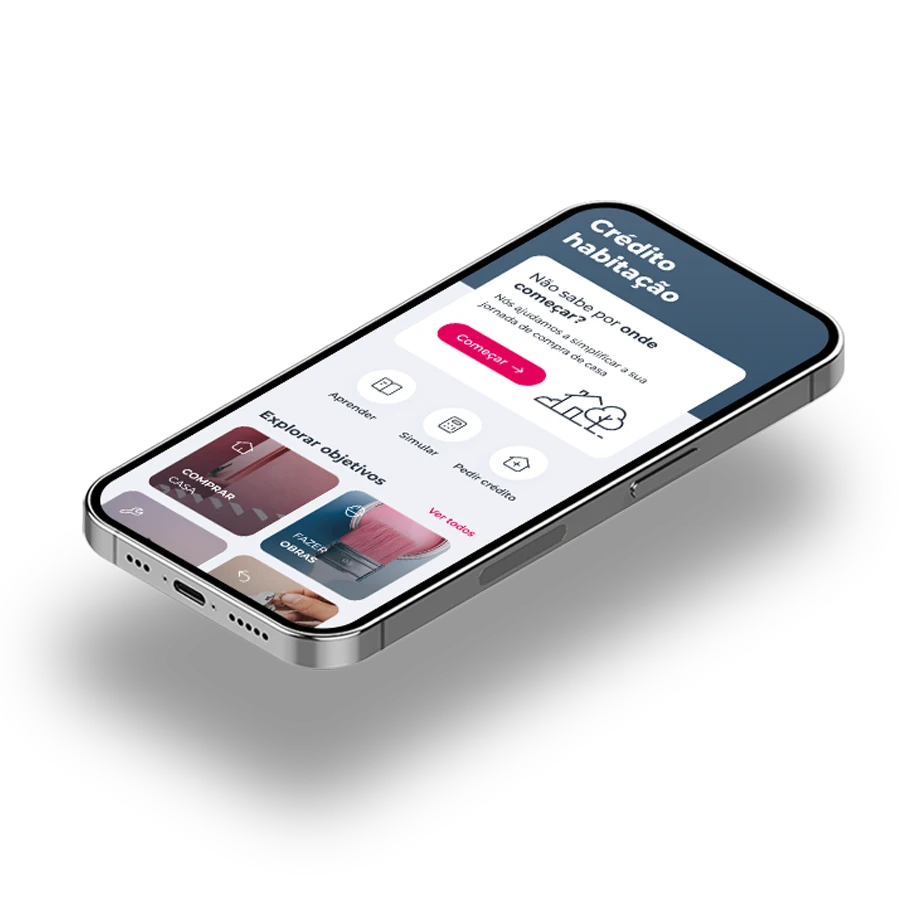

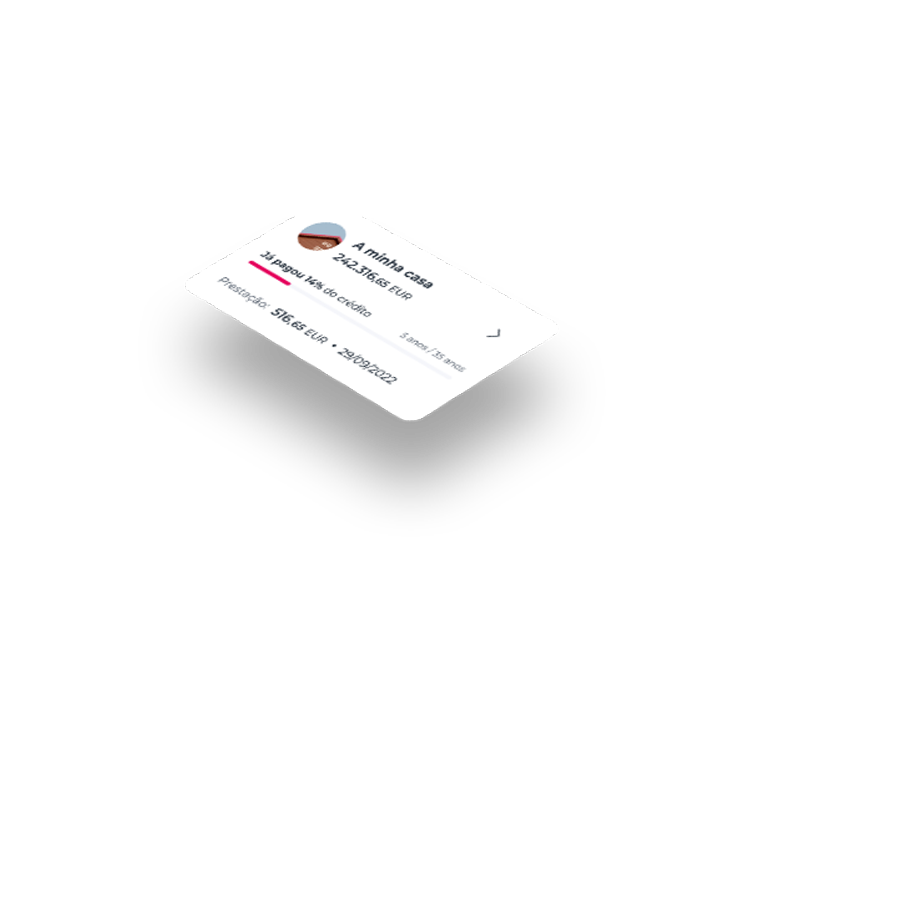

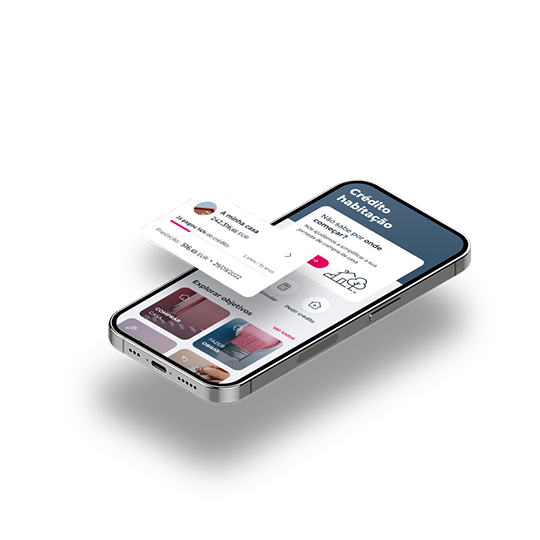

Mortgage loan

I need a mortgage loan...

Mortgage Loan Solutions

Zero has never been worth more

Loan subject to approval

Loan subject to approval

Conditions valid for proposals approved until 30/09/2026 and hired until 31/10/2026

Conditions valid for proposals approved until 30/09/2026 and hired until 31/10/2026

Loan subject to approval

Loan subject to approval

Conditions valid for proposals approved until 30/09/2026 and hired until 31/10/2026

Conditions valid for proposals approved until 30/09/2026 and hired until 31/10/2026

Buy a house

This is your new home,

Fixed rate solutions

Discounts for efficient homes

House renovations

Refurbish your home the way it deserves

Pay less during works

Exclusive partners

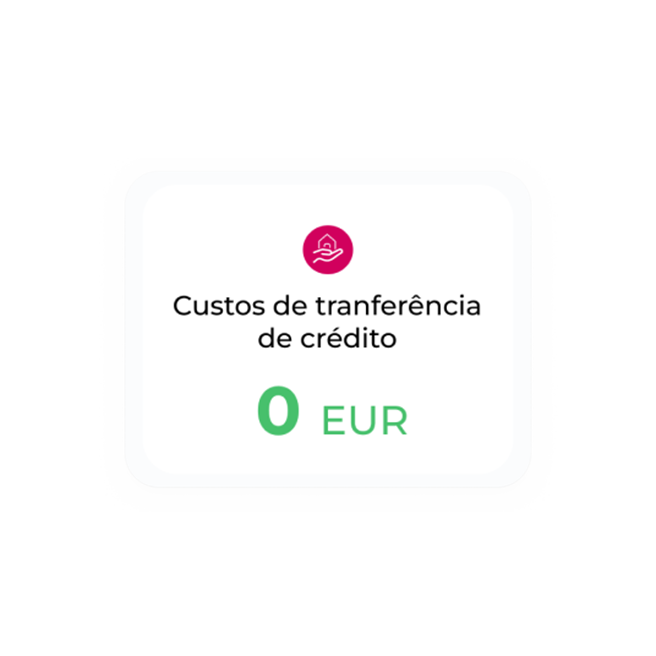

Transfer Mortgage Loan

Bring your mortgage to Millennium

Exemption from expenses

Exclusive partners

Build a house

Build the home of your dreams

Sustainable loan

Exclusive partners

Different purposes

For other goals you might have

Exclusive partners

Flexibility in the deed

Subsidized Loan for people with disabilities 1.8% TAEG

With subsidized rate

Capital repayment from day one

Life insurance not mandatory

Compare cards

If You’re Young

What are you waiting for?

State Personal Guarantee

IMT And Stamp Duty Exemption

Premium service

No red tape. We take care of everything

Don't waste time, we collect all the necessary documentation

More flexibility to sign the deed, available on weekdays until 10pm and Saturdays from 9am to 12pm

If you can't be present, we can represent you at the signing

Insurance, responsability, and more

Get your mortgage with...

Get discounts and benefits

Know how much you can apply for?

Mortgage at another Bank?

Protect your home with HOMIN insurance

Discover our offer

With the mortgage life insurance

Protect your home with seguro HOMIN

We ensure your monthly loan payments

Learn what happens in case of credit agreement default

Learn how the Financial Follow Up service works

Awards and Distinctions

Fastest Process, Most Digital Bank, and Best Mortgage Transfer Campaign

Fastest Process

Millennium bcp was distinguished in the 2025 Summer Mortgage Loan Awards by ComparaJá.pt in the “Fastest Process” category, having been the Bank that most streamlined the credit process for Consumers who used ComparaJá’s services. This distinction is only possible thanks to the dedication and professionalism of the extensive team involved in the various stages of the mortgage loan process.

Most Digital Bank

Millennium bcp was distinguished in the 2025 Summer Mortgage Loan Awards by ComparaJá.pt in the “Most Digital Bank” category for offering innovative and practical digital solutions, ensuring an efficient and intuitive online experience throughout the summer. This distinction is only possible thanks to the dedication and professionalism of the extensive team involved in the various stages of the mortgage loan process.

Best Mortgage Transfer Campaign

Millennium bcp was distinguished in the 2025 Summer Mortgage Loan Awards by ComparaJá.pt in the “Best Credit Transfer Campaign” category, having presented the best transfer campaign and achieving the best scores in ComparaJá’s analysis. This distinction is only possible thanks to the dedication and professionalism of the extensive team involved in the various stages of the mortgage loan process.

These awards are the sole responsibility of the entities that granted them.

Awards and Distinctions

Fastest Process, Most Digital Bank, and Best Mortgage Transfer Campaign

Fastest Process

Millennium bcp was distinguished in the 2025 Summer Mortgage Loan Awards by ComparaJá.pt in the “Fastest Process” category, having been the Bank that most streamlined the credit process for Consumers who used ComparaJá’s services. This distinction is only possible thanks to the dedication and professionalism of the extensive team involved in the various stages of the mortgage loan process.

Most Digital Bank

Millennium bcp was distinguished in the 2025 Summer Mortgage Loan Awards by ComparaJá.pt in the “Most Digital Bank” category for offering innovative and practical digital solutions, ensuring an efficient and intuitive online experience throughout the summer. This distinction is only possible thanks to the dedication and professionalism of the extensive team involved in the various stages of the mortgage loan process.

Best Mortgage Transfer Campaign

Millennium bcp was distinguished in the 2025 Summer Mortgage Loan Awards by ComparaJá.pt in the “Best Credit Transfer Campaign” category, having presented the best transfer campaign and achieving the best scores in ComparaJá’s analysis. This distinction is only possible thanks to the dedication and professionalism of the extensive team involved in the various stages of the mortgage loan process.

These awards are the sole responsibility of the entities that granted them.

Want to apply for a mortgage loan?

Before you make a decision...

Need help?

Need help?

Looking for a branch?

Looking for a branch?

Need to call us?

Need to call us?