Reforma Ativa PPR 2.ª Série

From €30 with tax benefits up to €400/year

This retirement plan serves as an additional support, bridging the gap between your final paycheck and your retirement income

Benefits

Why invest in this retirement plan?

Your money is always available under the conditions provided by law

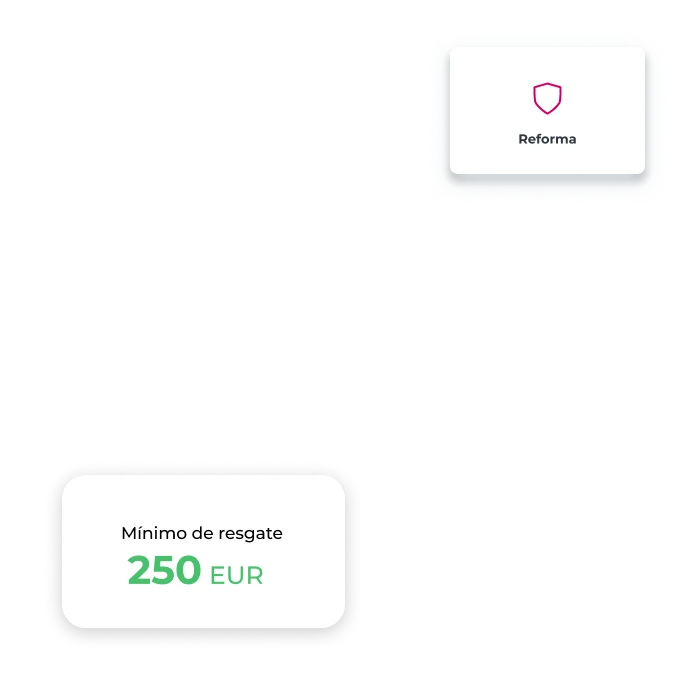

You can redeem your PPR at any time with a minimum amount of €250

You can deduct up to 20% on IRS of the money you invest on your PPR annually

Reduce your taxes over income from 28% to a minimum of 8%

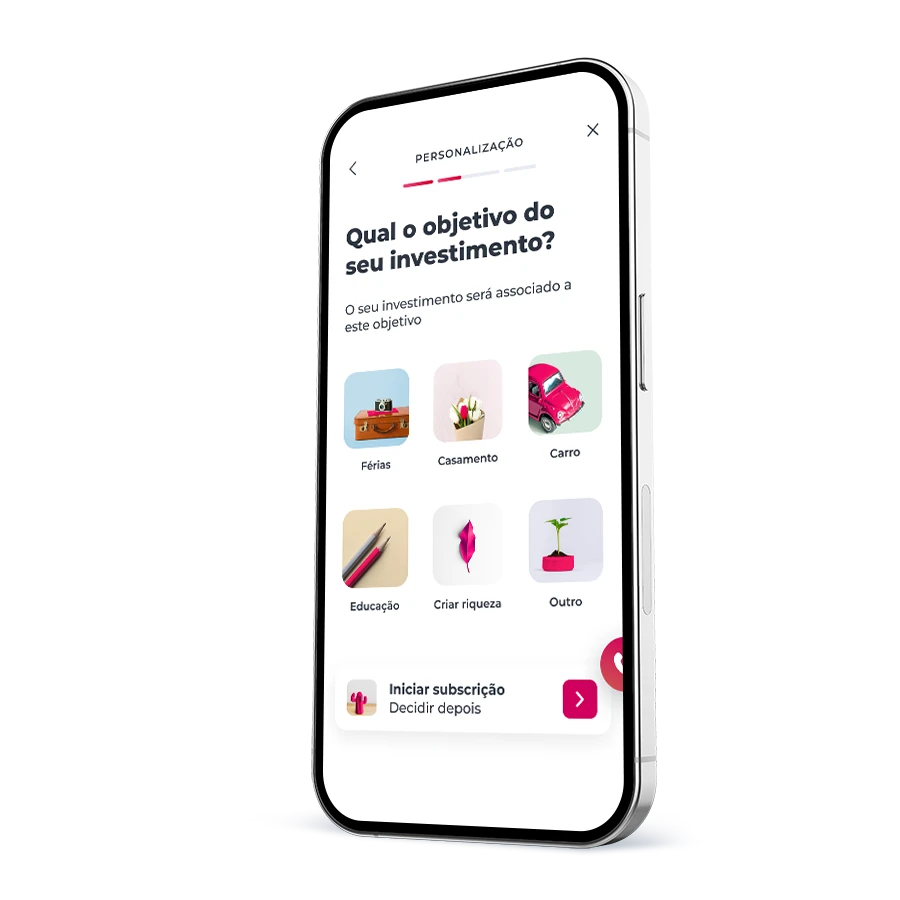

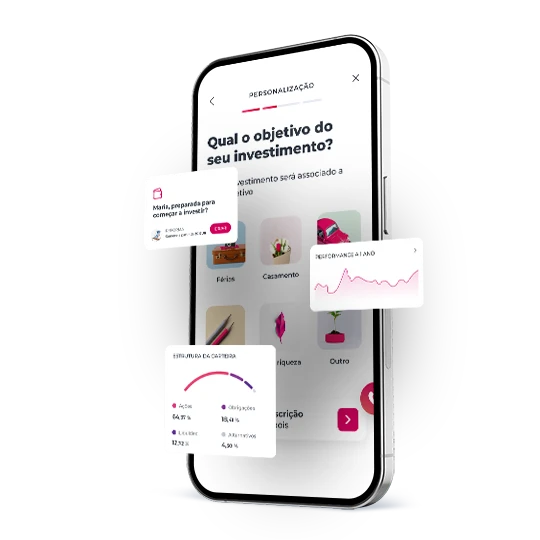

Customizable and 100% digital

You can choose between two investment options: Life cycle or Free choice

Your money is always available under the conditions provided by law

You can redeem your PPR at any time with a minimum amount of €250

You can deduct up to 20% on IRS of the money you invest on your PPR annually

Reduce your taxes over income from 28% to a minimum of 8%

Customizable and 100% digital

You can choose between two investment options: Life cycle or Free choice

Allocation strategies

Invest with one of these strategies

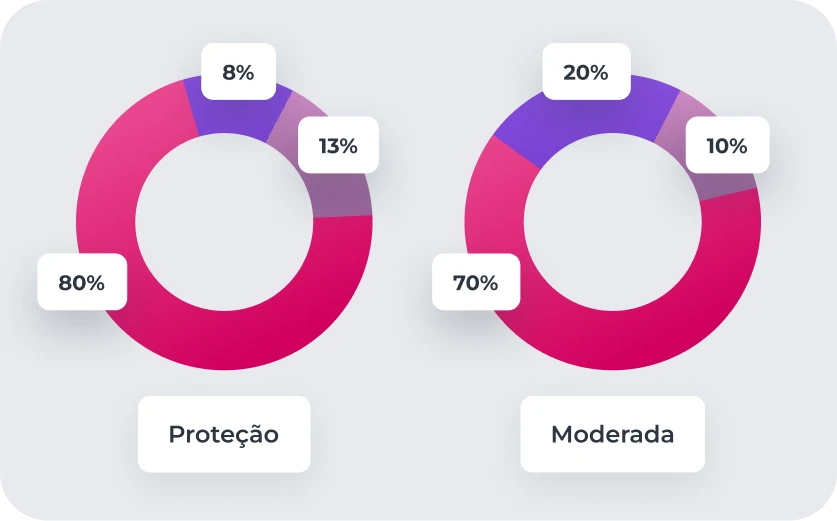

The Protection Strategy has low risk and a maximum limit of 10% stocks

The Moderate Strategy has medium to low risk and a maximum limit of 30% stocks

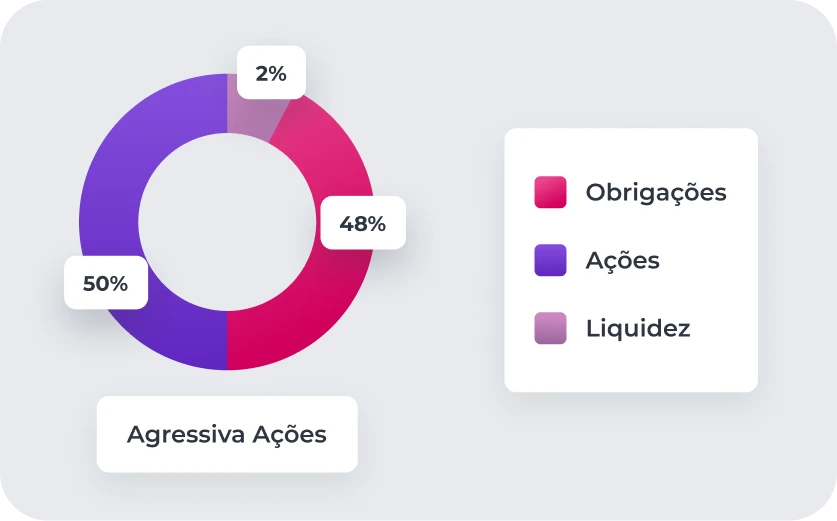

The Aggressive Stocks Strategy has medium risk and a maximum limit of 55% stocks

Investment options

Tailored to your needs

Life cycle

Managed according to your age

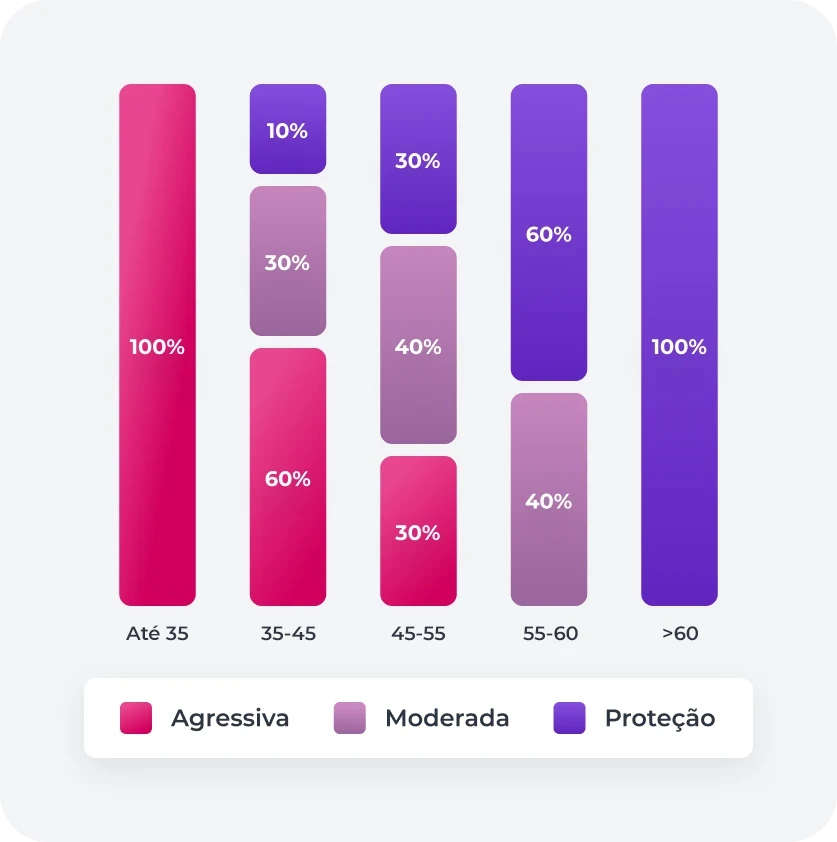

Our experts allocate deliveries to each of the strategies according to your age. Up to the age of 35, the strategies with the highest risk are chosen. And as time goes by, deliveries are assigned to the strategies with less risk.

Free choice

Decide how to distribute the deliveries

Choose the distribution of deliveries to each of the different strategies, according to your investment preferences. You can choose more than one strategy, allocating partial amounts of your delivery to different strategies.

1, 2, 3 and that’s it!

Preparing for retirement has never been this easy

Log in

Log in

and go to For you > Invest

and go to For you > Invest

Select the option Retirement

Select the option Retirement

Calculate and subscribe

Calculate and subscribe

after reading and accepting the legal documents

after reading and accepting the legal documents

What do you need?

What do you need?

To be over 18 years old

To be over 18 years old

To have a tax address in Portugal

To have a tax address in Portugal

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Calculate

Calculate

your retirement income considering your salary, savings, and goals

your retirement income considering your salary, savings, and goals

Log in

Log in

and fill in your personal details to continue the subscription

and fill in your personal details to continue the subscription

Subscribe

Subscribe

after reading and accepting the legal documents

after reading and accepting the legal documents

What do you need?

What do you need?

To be over 18 years old

To be over 18 years old

To have a tax address in Portugal

To have a tax address in Portugal

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

1, 2, 3 and that’s it!

Preparing for retirement has never been this easy

Log in

Log in

and go to For you > Invest

and go to For you > Invest

Select the option Retirement

Select the option Retirement

Calculate and subscribe

Calculate and subscribe

after reading and accepting the legal documents

after reading and accepting the legal documents

What do you need?

What do you need?

To be over 18 years old

To be over 18 years old

To have a tax address in Portugal

To have a tax address in Portugal

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Calculate

Calculate

your retirement income considering your salary, savings, and goals

your retirement income considering your salary, savings, and goals

Log in

Log in

and fill in your personal details to continue the subscription

and fill in your personal details to continue the subscription

Subscribe

Subscribe

after reading and accepting the legal documents

after reading and accepting the legal documents

What do you need?

What do you need?

To be over 18 years old

To be over 18 years old

To have a tax address in Portugal

To have a tax address in Portugal

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Answer the Investor Questionnaire, if you haven't already done so, to find out which products are right for you

Related topics

Other options to prepare your retirement

Seguro Investidor Global 2ª Série

Seguro Investidor Global 2ª Série

Investments adapted to your risk profile

Investments adapted to your risk profile

PPR funds calculator

PPR funds calculator

Start planning your future projects

Start planning your future projects

IMGA Poupança PPR

IMGA Poupança PPR

Value your savings with low risk tolerance

Value your savings with low risk tolerance

IMGA Investimento PPR

IMGA Investimento PPR

Value your savings with no risk tolerance

Value your savings with no risk tolerance

Seguro Investidor Global 2ª Série

Seguro Investidor Global 2ª Série

Investments adapted to your risk profile

Investments adapted to your risk profile

PPR funds calculator

PPR funds calculator

Start planning your future projects

Start planning your future projects

IMGA Poupança PPR

IMGA Poupança PPR

Value your savings with low risk tolerance

Value your savings with low risk tolerance

IMGA Investimento PPR

IMGA Investimento PPR

Value your savings with no risk tolerance

Value your savings with no risk tolerance

Need help?

Need help?

Looking for a branch?

Looking for a branch?

Need to call us?

Need to call us?