Financial Insurances

Explore our financial insurance options

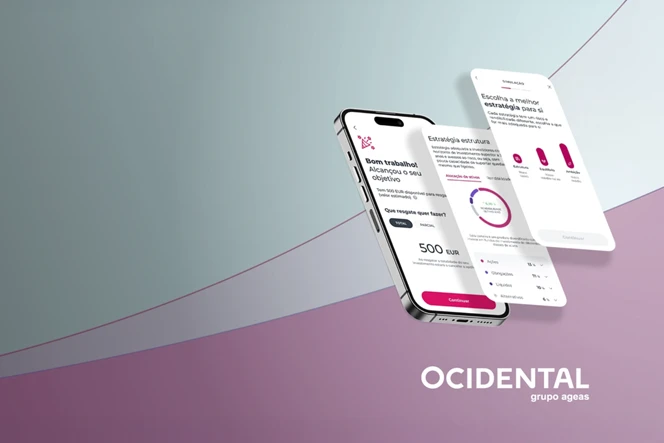

Reforma Ativa PPR 2.ª Série

From €30

Invest in an insurance managed by specialists

Invest in an insurance managed by specialists

Enjoy up to €400 on tax benefits

Enjoy up to €400 on tax benefits

Invest in an insurance managed by specialists

Invest in an insurance managed by specialists

Enjoy up to €400 on tax benefits

Enjoy up to €400 on tax benefits

Seguro Investidor Global 2.ª Série

Invest with 5 investment strategies

Risk Life Insurance

Tax benefits

Easy Invest

Invest on auto-pilot with the

3 strategies

Tax benefits

Compare cards

How does financial insurance work?

Insurance products linked to funds, expertly managed for customized and flexible investment solutions.

As long as you comply with the legal requirements.

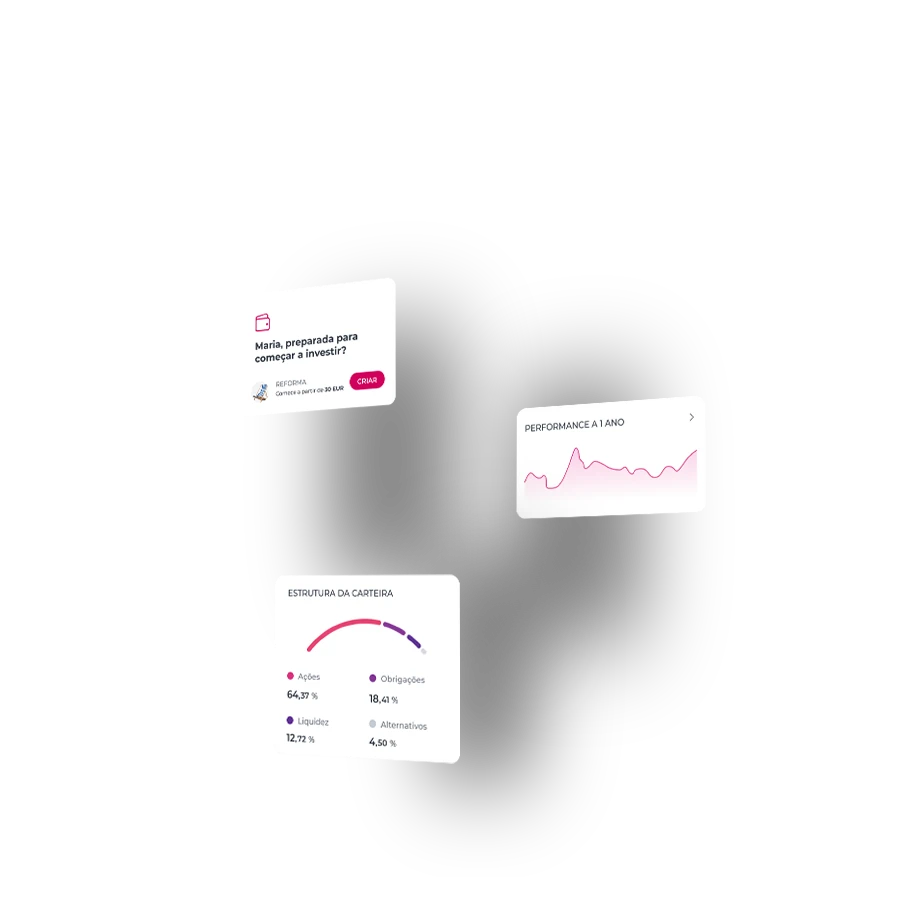

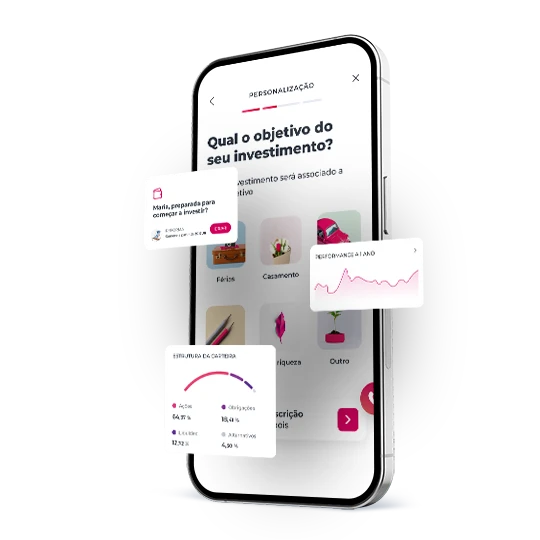

Each funds is linked to a diversified portfolio.

Our diverse range of funds, each with varying risks and returns, can be easily tailored to suit your needs.

You can get tax benefits when you redeem a financial insurance or when it terminates, from 11,2% to 28%.

Invest in 4 steps!

It’s that easy!

Login to the website

Login to the website

and choose the product to start investing.

and choose the product to start investing.

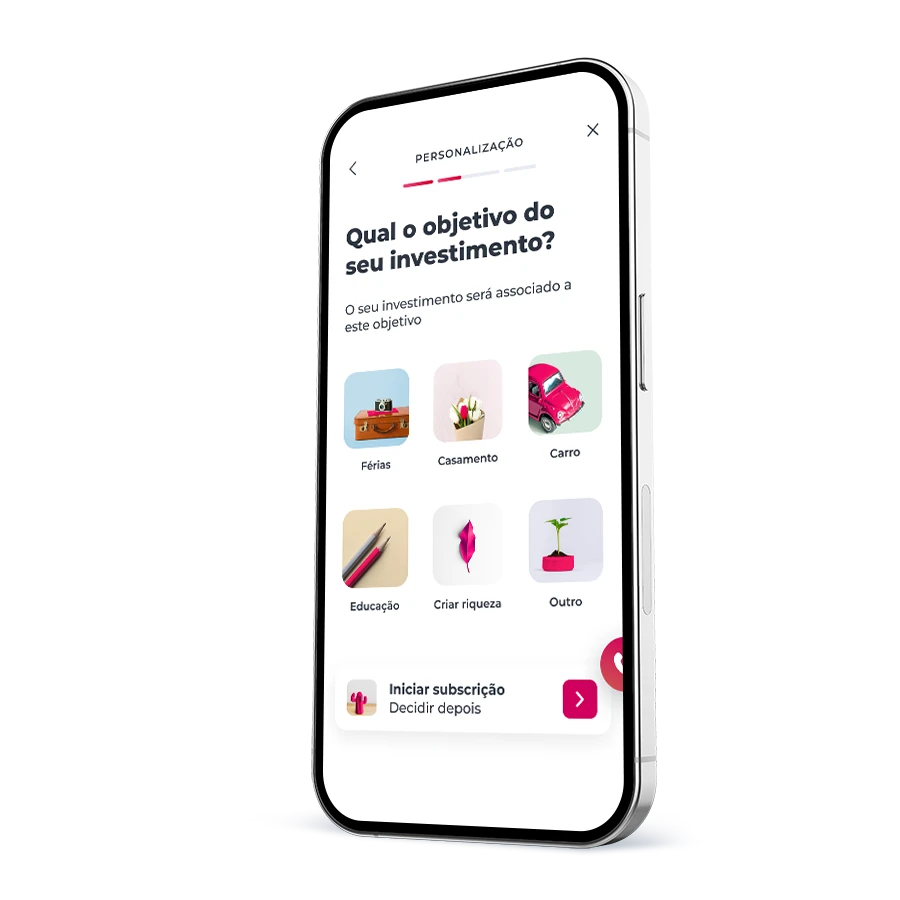

Choose the insurance

Choose the insurance

that best suits your needs and goals.

that best suits your needs and goals.

Calculate the investment

Calculate the investment

by filling out the necessary details.

by filling out the necessary details.

Confirm the subscription

Confirm the subscription

after reading the legal documents and confirming the operation details.

after reading the legal documents and confirming the operation details.

What do you need?

What do you need?

To be over 18 years old

To be over 18 years old

To fill out the Investor Questionnaire so that you know which products you can buy

To fill out the Investor Questionnaire so that you know which products you can buy

Invest in 4 steps!

It’s that easy!

Login to the website

Login to the website

and choose the product to start investing.

and choose the product to start investing.

Choose the insurance

Choose the insurance

that best suits your needs and goals.

that best suits your needs and goals.

Calculate the investment

Calculate the investment

by filling out the necessary details.

by filling out the necessary details.

Confirm the subscription

Confirm the subscription

after reading the legal documents and confirming the operation details.

after reading the legal documents and confirming the operation details.

What do you need?

What do you need?

To be over 18 years old

To be over 18 years old

To fill out the Investor Questionnaire so that you know which products you can buy

To fill out the Investor Questionnaire so that you know which products you can buy

Related topics

Some more investment picks...

Reforma Ativa PPR 2ª Série

Reforma Ativa PPR 2ª Série

Get up to €400 deduction on your tax return

Get up to €400 deduction on your tax return

Investment funds

Investment funds

Access several markets with a single investment

Access several markets with a single investment

ETF (Exchange-Traded Fund)

ETF (Exchange-Traded Fund)

For a low-cost diversified risk portfolio

For a low-cost diversified risk portfolio

Certificates

Certificates

Traded in the stock market and managed by experts

Traded in the stock market and managed by experts

Reforma Ativa PPR 2ª Série

Reforma Ativa PPR 2ª Série

Get up to €400 deduction on your tax return

Get up to €400 deduction on your tax return

Investment funds

Investment funds

Access several markets with a single investment

Access several markets with a single investment

ETF (Exchange-Traded Fund)

ETF (Exchange-Traded Fund)

For a low-cost diversified risk portfolio

For a low-cost diversified risk portfolio

Certificates

Certificates

Traded in the stock market and managed by experts

Traded in the stock market and managed by experts

Need help?

Need help?

Looking for a branch?

Looking for a branch?

Need to call us?

Need to call us?